IR35 for Contractors

HMRC introduced IR35 (or the ‘Off-Payroll Working Rules’) in 2000 to fight back against what it calls ‘disguised employment’. The IR35 legislation is designed to determine whether a Contractor is genuine rather than a ‘Disguised Employee’, for tax purposes.

IR35 legislation ensures that a “Disguised Employee” will be deemed ‘Inside IR35’ and will pay the same Tax and National Insurance contributions as an equivalent Employee.

To be deemed ‘Outside IR35’ means satisfying complex HMRC criteria to prove operation as a genuine business, and therefore operating outside of the IR35 rules.

What is changing?

Off-Payroll reform brings IR35 legislation in the private sector in line with the public sector. The Contractor shall no longer be responsible for assessing status and neither will the Contractor be responsible for the Tax due to HMRC.

Instead, new legislation (as per Chapter 10 ITEPA 2003) transfers the responsibility of assessing status from the Contractor to the Medium or Large Size End Client (size defined as per the Companies Act 2006 s382).

As well as the responsibility transferring, the tax liability will now rest with the deemed employer (or fee-payer) that is closest to the Contractor’s limited company.

What should I do now?

- Act NOW

- Assess your current contingency workforce / future contingency hiring plans

- Partner with a Technology Recruitment Agency with demonstrated IR35 expertise

The cost of getting IR35 wrong

With the changes to IR35, liability shifts to the Fee Payer when engaging a Contractor. It is now the responsibility of your business to determine if they fall inside or outside IR35. Not only will this be time consuming, but issues can arise from lack of IR35 knowledge in your HR Team / Hiring Managers.

According to Kingsbridge’s expert IR35 Legal Team, if due care and attention is not given to these status determinations (for example, if blanket or role-based determinations are made), then the Hiring Organisation (not the fee-payer) becomes liable for any unpaid tax and the legal and financial headache that comes with sorting this out. The fee payer is responsible where reasonable care can be demonstrated.

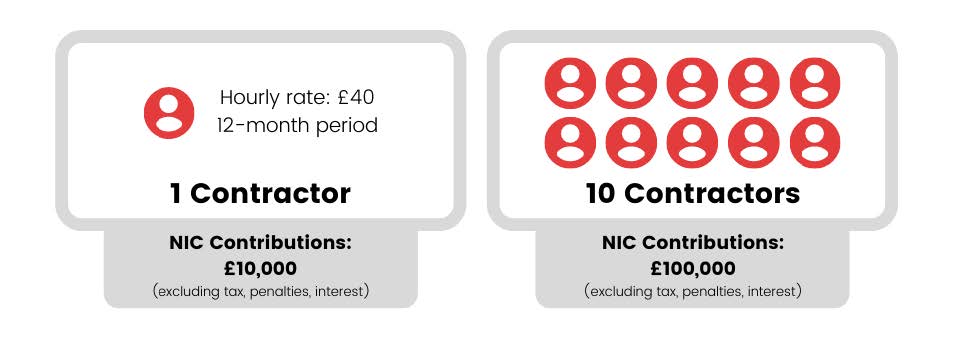

An example of getting it wrong

Aside from the financial risk, it is vitally important to be properly prepared when assessing IR35 determinations, due to the risk of a Talent Drain. Recent research has found that 61% of Contractors would look for another role if incorrectly assessed.

Blanket ban or assessment?

You might be thinking, “there’s too much risk involved, I’ll just put a blanket ban on Limited Company / PSC Contractors” regardless of their individual circumstances, or you might decide to blanket assess your contingent workforce.

- HMRC have said Blanket Assessments might not meet the reasonable care test if true circumstances are not considered.

- Companies who fairly assess IR35 compliance will be more attractive to genuine Technology Contractors vs. those who do not.

Why not just use the CEST tool?

HMRC’s Check Employment Status for Tax (CEST) tool has been widely declared inaccurate and unreliable. HMRC themselves have routinely refused to stand over determinations reached by CEST. In 2019 NHS Digital was hit with a £4.3m tax bill as a direct result of the IR35 status determinations it carried out using CEST.

What about other automated IR35 determination tools?

There are an increasing amount of online automated IR35 determination tools available, but:

- Borderline status determinations that do not provide a clear answer on status require manual and/or legal intervention

- Their determinations are generally not backed by a comprehensive insurance policy

- There is the potential of bogus or unproven tools that leave you open to risk